| مشخصات مقاله پاورپوینت انگلیسی |

| عنوان فارسی مقاله |

هزینه یابی هدف |

| عنوان انگلیسی مقاله |

Target Costing |

| فرمت مقاله |

پاورپوینت (PPT یا PPTX) |

| تعداد اسلایدها |

16 اسلاید |

| قابلیت ویرایش |

دارد |

| قابلیت پرینت |

دارد |

| رشته های مرتبط با این مقاله |

مدیریت و علوم اقتصادی |

| گرایش های مرتبط با این مقاله |

مدیریت مالی، اقتصادی مالی و مدیریت استراتژیک |

| کد محصول |

EP93 |

دانلود رایگان پاورپوینت انگلیسی سفارش ترجمه این پاورپوینت

| تصویری از مقاله |

|

| فهرست مطالب |

|

Target Costing

Training Overview

What is Target Costing?

Brainstorming Exercise

Goal of Target Costing

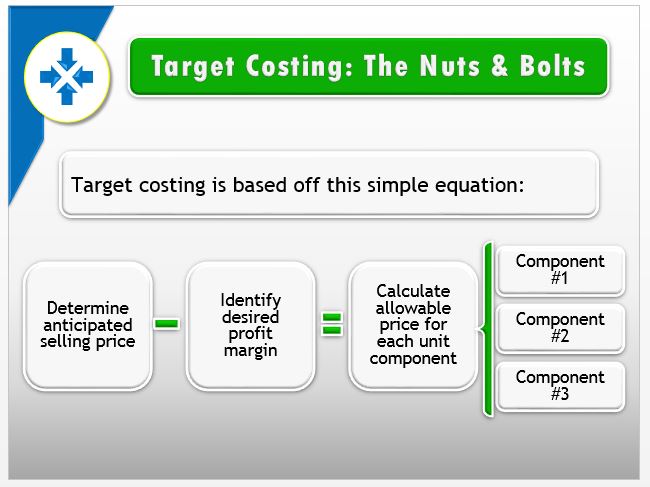

Target Costing: The Nuts & Bolts

How it Works – Overview

How it Works – Part 1 – Analysis

How it Works – Part 2- Design

How it Works – Part 3 – Implement

Real World Example

Now It’s Your Turn

Now It’s Your Turn – Solution

Review & Summary

Reading List & Further Research

Sources

|

| بخشی از مقاله |

|

Real World Example

In Business | Target Costing Approach–An Iterative Process:

Target costing Technique is widely used in Japan. In the automobile industry, the target cost for a new model is decomposed into target costs for each of the elements of the car–down to a target cost for each of the individual parts. The designers draft a trial blueprint, and a check is made to see if the estimated cost of the car is within reasonable distance of the target cost. If not, design changes are made, and a new trial blueprint is drawn up. This process continues until there is sufficient confidence in the design to make a prototype car according to the trial blueprint. If there is still a gap between the target cost and estimated cost, the design of the car will be further modified.

After repeating this process a number of times, the final blueprint is drawn up and turned over to the production department. In the first several months of production, the target costs will ordinarily not be achieved due to problems in getting a new model into production. However after that initial period, target costs are compared to actual costs and discrepancies between the two are investigated with the aim of eliminating the discrepancies and achieving target costs.

Source: Yasuhiro Monden and Kazuki Hamada, “Target Costing-Kaizen Costing in Japanese Automobile Companies,” Journal of Management Accounting Research 3, pp. 16-34.

|

دانلود رایگان پاورپوینت انگلیسی سفارش ترجمه این پاورپوینت